I was getting bored in class the other day, so I did what I usually do when I start to research a stock; I went to the SEC company database and looked up their financial statements. I then proceeded to fall down a sort of rabbit hole of accounting, to do with the ability of a company to issue more Equity (stock) and suddenly be worth more money. This post will be my endeavor to explain my thoughts, and to put them in context with some Due Diligence of the terrible excuse of a company I researched.

First, let’s go over the basics of accounting. Accounting is the universal language of business, and though the dialect of that language may change in different parts of the world, the fundamentals are simple. There is one equation that builds a business, and it is the same for every business:

Assets = Liabilities + Equity

Defining the terms…

Assets are the parts of a company that generate money. This ranges from Cash and Investments, to Land and Buildings, to Patents and Copyrights.

Liabilities are the parts of a company that lose money. Debt goes in this category, as well as any income taken in advance.

Equity, in simple terms, is what’s left. This is where the company stores its money. The Initial Value of issued Stock goes in this category, and any profit/loss from the year’s operations go in the Retained Earnings account in this category as well. The third most important account here is Additional Paid In Capital, the account that grows when the company issues more shares of stock.

Accounting uses the Double-Entry system, meaning an addition or subtraction from one half of the above equation must be matched with an equal change from the other half. For example, say my company bought a new car worth $20,000 with a $4,000 down payment and a $16,000 auto loan:

Assets = Liabilities + Equity

+$20,000 + $16,000 +$4,000

Assets goes up by the value of the car, while Liabilities and Equity go up by the same amount, broken up by the value of the loan and down payment, respectively.

The two sides to this equation must balance at all times. Failure to balance isn’t necessarily breaking any rule or regulation, but it means the financial statements don’t accurately reflect the standing of the company it describes.

The company I was looking at, the company I love to chastise, is Advanced Micro Devices, or AMD. You may recognize the name, they are a chipmaker and a competitor of Intel and Nvidia. I should say for emphasis that both Intel and Nvidia are profitable. AMD posted a profit of 7 cents per share on just over 1 billion shares of their stock, or $70 million this past quarter. Let’s see if that number is really accurate.

AMD is, to quote a friend, the textbook definition of a memestock. They make chips that are used to mine cryptocurrency, and they’ve had a few other big headlines, and as a result, millions more shares of AMD get traded each day relative to other stocks in its industry. But this stock, as I will hopefully explain to you in clear enough terms, is a dumpster fire. To quote Gordon Gekko from the classic movie Wall Street, it’s dogshit.

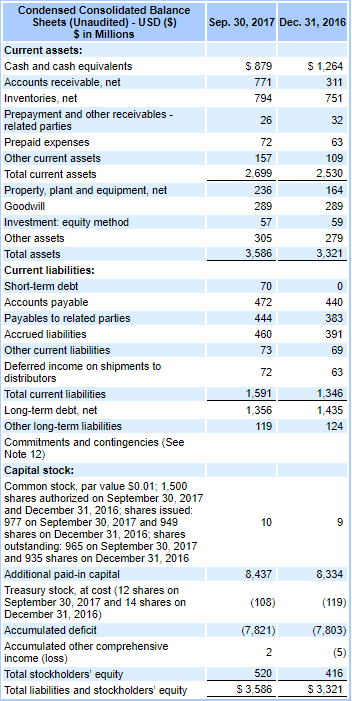

Below is a snapshot of AMD’s Balance Sheet from the most recent quarter. Notice that the accounting equation shown above holds up.

A few observations to glean from this statement. Total Liabilities are about the same amount as Total Assets, which is very unusual for a tech company. But at the bottom, where the Equity section would go, their Accumulated Deficit account is tremendously negative, to the tune of $7.8 billion. This is the account that contains the sum of all their profits or losses, and from the look of their balance sheet, they have a lot of losses. This is directly offset by their Additional Paid In Capital account, valued at $8.4 billion, and providing almost the entirety of their Total Equity of $520 million.

Why is their APIC so high? That account can only be so high if AMD issues a lot more equity, no? Let’s dig a little deeper. Keep in mind that the accounting equation must balance, so if AMD issues $1 million worth of equity, they can report $1 million of cash to balance it out.

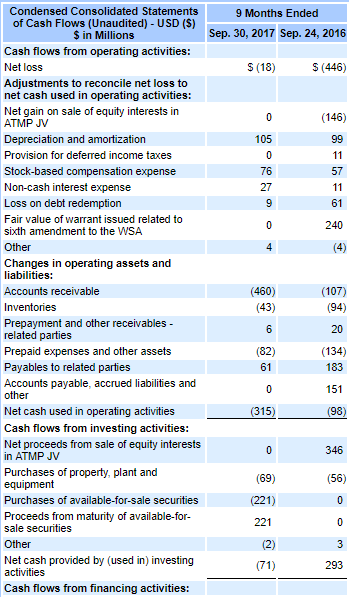

Below is AMD’s most recent Statement of Cash Flows. This statement takes their bottom line (net income) and breaks out the noncash factors to see how money really moves. Money, or lack thereof.

Let’s work our way down this statement to see the important things. First, AMD posted a net loss of $18 million this quarter, but issued $76 million of stock-based compensation. Warren Buffett would call this a red flag of financial disclosure. Normally, you would think, compensation is shown as a cash expense, meaning employees get paid with money. That would be recorded as a subtraction of Cash (on the Asset side of the accounting equation) and an increased wage expense, shown as a lowering of Retained Earnings (on the Liabilities + Equity side). Paying your employees in stock is not a huge deal, as long as it is recorded as an expense. When it is not an expense, then it is used to prop up earnings as equity accounts are increased, but not decreased.

Now that we understand that issuing equity to pay for things without including it in expenses is bad, look at the bottom of the sheet. You will see that AMD issued $38 million worth of stock to pay for their debt. This is not recorded as an expense, rather it is effectively canceling debt by issuing equity. If I understand this transaction correctly, they settle debt in stock, that is worth cash, meaning their Assets go up by the amount of money raised by issuing stock, and their Liabilities + Equity side remains the same by substituting debt for stock. This overstates their assets and lies to shareholders. If we subtract the $38 million in issued stock from the reported income of $70 million, we are left with $32 million. If we further subtract out the proceeds from issuance of stock from stock-based compensation as a financing activity, we are left with $23 million. Lastly, look at the Accounts Receivable line. This is where money that is acknowledged as revenue, but hasn’t come in yet (possibly due to terms on a contract or an accounting method) is recorded. If we take that into account, cash net income is profoundly negative, but we’ll leave that be.

Let’s move on.

Below is a snapshot of AMD’s note to its stock-based compensation plans for the recent quarter and nine month fiscal year so far.

You can see that AMD issued another 8.3 million shares of stock as part of compensation, at a value of $13.24. This comes out to $109 million in cash raised for this quarter in just this area of equity issuance. While this makes accounting sense, as I said earlier, from a point of view of a potential investor, this should raise a huge alarm! AMD only made $23 million in the current quarter, yet they issued nearly 4 times that amount in just stock-based compensation! That should immediately tell you that AMD cares about paying its management more than it cares about turning a decent profit, or returning capital to its shareholders.

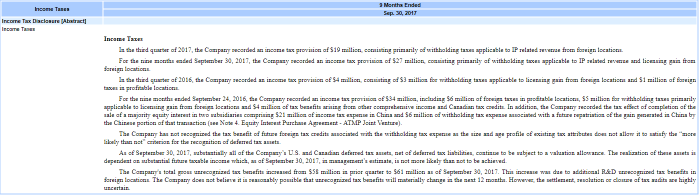

The last item I want to look at comes from their financial statement note regarding their ability to pay income taxes.

Specifically in the second to last paragraph, AMD mentions that it has substantial deferred tax assets that have arisen from its losses in prior years. These deferred tax assets are Net Operating Losses that are accrued to the company when it doesn’t turn a profit. Instead of a direct payment from the government, this NOL can carry forward indefinitely to offset future gain. However, AMD states that “The realization of these assets is dependent on substantial future taxable income which, as of September 30, 2017, is management’s estimate, is not more likely than not to be achieved.” In lighter terms, AMD can offset those NOL’s with future gain, but management does not anticipate enough gain to materially make use of the NOL’s.

If that isn’t management saying they don’t expect to make any money, I don’t know what is. They say that, while they take home $109 million in company stock in just this last quarter. Insanity.

So, after all this, we know that AMD is barely profitable, if at all, and that they are only able to stay afloat by issuing massive amounts of Equity (to pay their officers and to pay their debt). Does that seem sustainable to you? It certainly does not seem that way to me. AMD is the recipient of a few headlines that play into all the market’s volatility (which as of writing this blog is in cryptocurrency) and the fanboys in that space trade this stock like it’s the next Microsoft. As a result, AMD is able to hold a price level of around $12-$13, despite having a Price/Earnings ratio of about 180. At that price point, with enough people still willing to buy this stock, management likely still feels that they can milk the company of its profitability while directly benefiting from Equity issuance to stay afloat. In this way, the company is essentially generating money out of thin air. At some point, there will either be too many shares outstanding to support the share price in the eyes of enough shareholders, or the company will run out of ways to pump out Equity, and the company will collapse unless it starts turning bigger profits. But who knows when that day will come.

If you read this far, I hope you were able to follow my thought process regarding AMD and some rigmarole of accounting! I will write in the future about how I screen a stock before buying it, and this is certainly part of that process. As always, if you have any questions, feel free to comment or send me an email, and as always, keep learning!

Pictures Taken From Source:

Discover more from The Millennial Economist

Subscribe to get the latest posts sent to your email.

Categories: Accounting, Finance

Insightful! Keep it up.

LikeLiked by 1 person

Thanks so much!

LikeLiked by 1 person

You really make it seem so easy together with your presentation however I find this topic to be really one thing that I believe I’d never understand. It sort of feels too complicated and very wide for me. I am taking a look ahead to your subsequent put up, I will try to get the dangle of it!

LikeLike

Thanks for reading! I believe that understanding a company’s financial information is as important as understanding its operations and image, this was just a little of how I look at a company. Every public company files quarterly reports on the SEC website I linked, check them out!

LikeLike

I’m no longer certain where you’re getting your information, but good topic. I must spend some time learning more or working out more. Thanks for excellent info I was on the lookout for this info for my mission.

LikeLike

Thnk you for reading!

LikeLike

Nice weblog here! Also your website quite a bit up very fast! What host are you using? Can I am getting your associate link for your host? I want my website loaded up as quickly as yours lol

LikeLike

Thank you so much! I use WordPress hosting, it’s pretty easy to choose a style that fits you or create your own.

LikeLike

Is it difficult to deal with what brings you money? What does it cost you?

LikeLike

Thanks for the comment! While not as difficult per se as work that brings in wage income. I believe a solid investment requires at least some knowledge of the company you choose for that investment, which takes time and effort.

LikeLike