Tomorrow, September 17th, 2025, the US Economy will officially* embark on the trajectory that trump has put forth.

The asterisk is present because we’ve unofficially been on the new trajectory for a period of months now, depending on who you ask. But tomorrow, it will be permanent and irreversible.

The President of the White House Council of Economic Advisors (CEA), Stephen Miran, has been confirmed by the Senate to sit on the Fed Board. Miran is a Harvard-educated economist who has previously served in Treasury positions. His qualifications are not in dispute. What is the subject of (my and other economists’) furor is the brazen attack on the Fed that his appointment represents.

Miran refused to step down from his political office in his Senate confirmation hearing, opting instead to take an “unpaid leave of absence” while he fills in the Fed Board seat of the recently-resigned Adriana Kugler. Effectively, he has told America that he does not plan to respect the Fed’s independence from political bias in fulfilling his duties as a voting FOMC member. His first day on the job is today, September 16th, when the Fed Board begins its 2-day interest-rate-setting meeting. Miran will have a vote in that process. Miran will also provide his input on the “dot plot”, a graphical measure of where the various Fed Board members believe data is headed in future months & years.

The Fed Board is a 12 member body, made up of 7 members who oversee overall Fed functions (such as Jerome Powell, the Chairman, and Christopher Waller, the Governor in charge of Reserve Banking and Payments Systems), as well as a rotating slate of 5 Governors of the 12 Federal Reserve regional banks. It is set up this way to ensure that there is a diversity of views from across the country discussed at every meeting.

It’s true that one vote out of a 12-member board is hardly consequential. But consider this as just one of many steps that trump is taking to remake the economy, and its guardrails, as he personally sees fit.

Consider another action trump is taking against the Fed, in attempting to fire “the Black one,” Fed Governor Lisa Cook, a leading international economist, early proponent of Endogenous Growth Theory, and the first Black woman to serve on the Fed Board. trump’s Federal Housing Finance Chief and lead financial attack dog Bill Pulte invented a charge of mortgage fraud against Cook, accusing her of securing loans for two homes while claiming both were her primary residence. The AP, Wall Street Journal, and Michigan State property appraiser have since debunked these false charges, showing via document filings that Cook’s second property was labeled a vacation home. That has not stopped trump and Pulte from “firing” Governor Cook, and it took a Federal Appeals Court today to say that Cook has not been fired and is able to fulfill her duties as a Fed Governor by sitting in this week’s policy meeting.

I don’t levy accusations of racism lightly, and definitely not without proof. But follow the facts with me. In a recent Supreme Court ruling, SCOTUS argued that the Federal Reserve is a “Quasi-private entity, in the vein of the First and Second National Banks,” and thus its leaders cannot be fired at the whim of the President. They have to be fired “for cause.” So the false charges are levied to give the pretense of cause, where there really isn’t any. And since they are made-up charges, trump could have levied them against any other member of the Fed Board, but he chose Governor Cook. It’s evident to me that he went after her specifically because she is Black.

Consider a third action trump has taken, this time against the country’s statistical agencies. In August, the Bureau of Labor Statistics (BLS) released the July jobs report, showing that job growth had drastically slowed, from a 2024 rate of over 100,000 jobs added per month, to a 2025 rate of just over 22,000 jobs added per month. Rather than attempt to understand the numbers and try to make them better, trump decided to fire the BLS Commissioner, Dr. Erika McEntarfer, for being the messenger of the bad news. His proposed nominee to fill her role, E.J. Antoni, an economist for the Heritage Foundation, promises to “fix” the numbers, and echoes trump’s claim that our country’s data collection agencies are “broken.”

There is some truth to this claim, especially when it comes to Jobs numbers. This is how the process works.

The BLS is mandated, on the first Friday of every month, to present the Jobs Report for the previous month. It accomplishes this by sending out two different surveys. One goes to households (the household survey) and the other goes to businesses (the establishment survey), sampling for between 60,000 and 180,000 participants for each survey. Based on that survey data, the BLS gets an estimate of how many jobs are added and how many are subtracted around the middle of every month, the data is smoothed for seasonal adjustment, and the smoothed estimates are published.

I call them estimates for good reason. These are surveys, not hard data, and surveys have a response rate of less than 100%. In recent months, the surveys have had a response rate of less than 60%, which causes the BLS to have to estimate more and more data. One benchmark the BLS uses to estimate is the “Birth-Death Model” which shows how many businesses are “born” and how many “die” in a given year. Business expansion theoretically means more job postings, which means more jobs. But you can probably see how this estimate can be skewed, for example, the birth of many Sole Proprietorships, for things like driving Uber or being an Economist (hello there!) mean there are fewer jobs being added than it may seem.

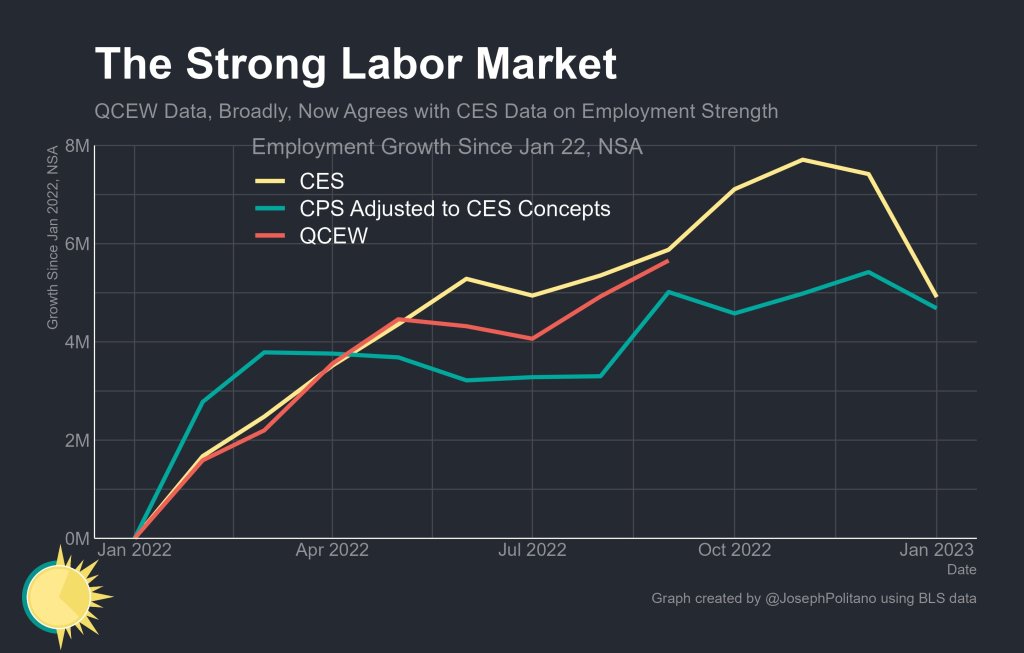

Every quarter, revisions to these estimates are benchmarked under what’s known as the QCEW – the Quarterly Concensus of Employment and Wages. Finally, this is the hard data we are searching for, in the form of IRS Forms 941 and various other quarterly tax filings, that show how many employers are actually at the businesses being surveyed, instead of just what is relayed via surveys. The previous three months’ data is checked against the hard tax data, and is revised to show the differences.

Sometimes the revisions are small, but sometimes they can be very large. It all depends on the quality of survey data collected, and thus the resources that go into collecting that data. This past month, the month after trump “killed the messenger” for giving him bad news, the news got even worse: the QCEW revisions to jobs data from March 2024 – March 2025 showed a downward revision of 911,000 jobs! That means that 911,000 fewer people were hired over the course of that time than the survery data showed. That’s a revision equivalent to 0.6% of the total US labor force; a small margin of error, but nonetheless a massive revision.

You might ask, if this is how it works, then why release monthly estimates at all?

The answer is pretty simple. Transparency is a good thing! More frequent data being released, coupled with a substantive process of refining that data, makes America a better place to invest in. People feel safe leaving their savings with us, because we offer them the transparency they need, to know exactly what is happening in the economy, to the best of our ability.

So clearly there is some room for improvement here. But is Antoni the right guy for the job? Or is he a trump stooge who would be installed just to rubber-stamp numbers that trump likes, reality to the wind? He has yet to be confirmed, and he has not given any concrete steps he would take to make data collection better, so at this time it’s too soon to tell. But we can speculate.

These are just three examples of how trump is attempting to change the makeup of our country’s “plumbing.” The apolitical, professional agencies that are responsible for keeping the economy going forward, suddenly now find themselves attacked by political biases, and risk succumbing to them.

Indeed, there is reason to worry. The US Economy is clearly weakening, as nearly all data suggests. The aforementioned QCEW, with its huge labor force revision, showed even worse numbers than we previously saw, showing that labor force growth had slowed from 150,000 jobs added per month in 2023, to 77,000 jobs added per month in 2024, to 22,000 jobs added per month in 2025. June’s jobs number was revised to the negative, meaning we lost more jobs than we gained that month.

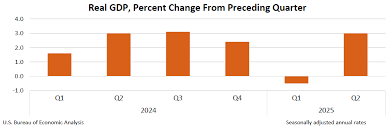

GDP, the measure of the total amount of goods and services produced in the country, has also weakened somewhat in 2025. As tariffs were levied, massive inventory buildups caused GDP to contract in the first quarter, before reversing and exploding higher in the second quarter. Trade data muddies the water, and we cant see a clear picture of the rest of the calculation just yet, but 2025 growth estimates from the CBO, big banks, the Fed, and nearly all reputable firms have dropped from the high 2% range in January, to the mid 1% range today. We shall see if they are correct.

GDP, by the way, gets its own revisions, the BEA publishing three GDP estimates for each quarter, each released one month after the last. For example, the second-quarter GDP, for the months April – June, gets three estimates, one in July, one in August, and one in September. We still do not have the September final estimate of Q2 GDP, and we won’t get Q3’s for another couple of months.

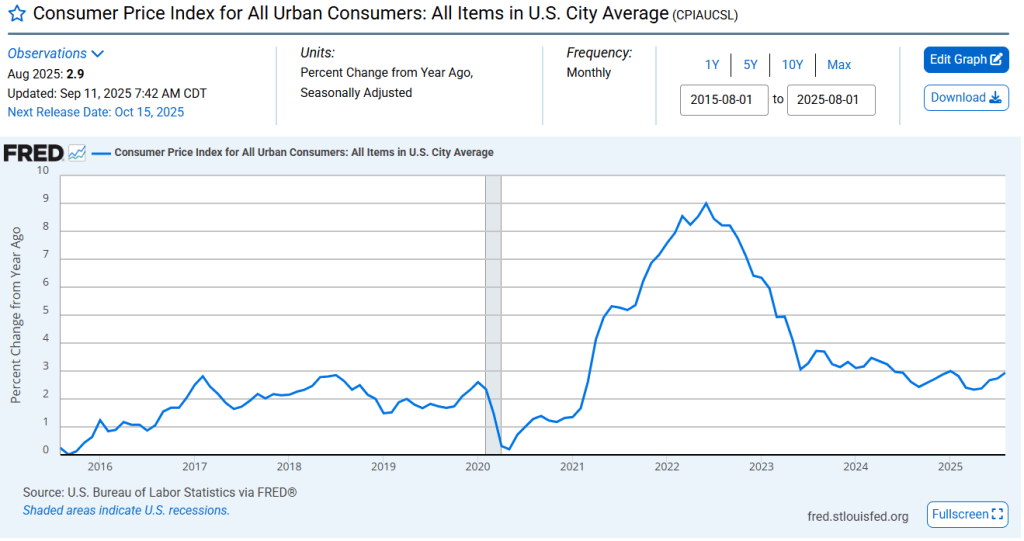

In the meantime, inflation continues to climb in the face of trump’s global tariff war. CPI inflation, a measure of the prices of goods found in stores, climbed back up to near 3% in August, far from the Fed’s baseline of 2%. You might expect this to be much higher, since tariff announcements have been so high, and so fickle. Firms have thus far been unwilling to pass on much of their tariff costs on to consumers, having experienced the bout of high inflation in 2021-22 and knowing how consumers felt about it. They want to keep their customer base, and who could blame them? But under the hood, the picture is far worse.

Large manufacturing companies, such as Ford, GM, and 3M, are factoring in billions of dollars in tariffs they must pay to the government. Smaller companies, that cannot absorb such large price hits, are bleeding themselves out of business. The recent Q2 earnings season shed some light on just how badly companies are taking it on the chin. Give a listen to some corporate earnings reports sometime, and you’ll see just how top of mind this is.

But just as the company’s scale affects the amount they have to pay, so does the company’s scale affect how much of a going concern their health is. Consider the performance of the S&P 500 compared to the Russell 2000, two indexes that show performance of publicly-traded companies. The S&P 500 represents the 500 biggest companies in America, and the Russell 2000 represents 2,000 smaller companies, far more indicative of the “real” American economy. Since January 1st, the S&P 500 has grown 12.4%, compared with the Russell 2000 growing just 6.9%. Normally, smaller-cap stocks have more upside, because their profits start at a much lower amount. Growing your profits from $10 billion to $11 billion represents a 10% growth rate, but growing from $1 billion to $2 billion represents a 100% growth rate, even if you only made $1 billion more in both scenarios. Stock prices are a reflection of a company’s growth, so small-caps should have higher growth rates. But tariffs are denting them.

Larger companies with larger cash hoards and the ability to wait and plan for higher prices, will eventually learn to live with them. Smaller companies, without that cushion, will suffer.

So on one hand, we have slowing job growth, showing weakness in the labor market. This calls for cutting interest rates, making borrowing easier, and juicing business expansion to hire more people. But on the other hand, we have rising inflation, showing weakness in real purchasing power. This calls for hiking interest rates, making borrowing harder, and lowering business expansion to control prices. The Fed has a Dual Mandate that is supposed to take both these factors into account, and for the first time in a good while, the two sides of the mandate are at odds with each other.

In late 2024, before recent labor market weakness and while inflation appeared to be in its last mile of moderation to the Fed’s goal of 2%, the Fed cut interest rates a few times. The two sides of the Dual Mandate were not at odds with each other, and while employment was holding up, inflation was the main focus. Price growth was returning to normal, so interest rates could as well. But in 2025, tariffs have injected a lot of uncertainty and have caused inflation to rise back up into painful territory, at the same time that employment has stalled out. There is no clear indication of what the Fed should do, so they have taken a wait-and-see approach, and have not raised or lowered interest rates from the January level of 4.25% – 4.50%.

I believe this is the correct thing to do, to wait and see how tariff inflation will shape prices. There are many factors that go into forecasting how things will shake out, as this website has reported in the past. Businesses stockpiled inventories at the start of the year to get ahead of tariffs, and even as those stockpiles run out, they are loathe to immediately pass on price increases to an increasingly stretched consumer. Recent guidance announcements from McDonald’s, Chipotle, and Cava illustrate this quite well. It remains to be seen just how tariff costs will flow through, but businesses will not accept a permanently lower margin, and thus a permanently higher stock multiple. Eventually, they will find their way into prices.

Right now, there is some reason for businesses to sit tight and accept temporarily lower margins. Moody’s Chief Economist Mark Zandi today released data showing that most Americans have experienced no spending growth, in real terms. The bottom 80% of American consumers have only increased their spending to the extent inflation has pushed prices up, meaning their spending is flat, and only the top 20% of Americans are spending any more money than they were last year. Clearly, the consumer is stretched, and cannot accommodate much more organic spending. They will be very sensitive to tariff price increases.

And to the labor side of the Fed’s Dual Mandate, other parts of trump’s agenda may be helping to solve that side of the problem. Job growth has slowed considerably, but there is reason to think that the mass deportations, and lack of immigration in 2025, has organically lowered the breakeven job growth number. Wendy Edelberg and Jed Kolko at the Peterson Institute took a look at the census, immigration, and payrolls data, and found that the breakeven monthly employment figure has fallen by about half, from 166,000 per month in early 2024, to just 86,000 in mid 2025. That is to say, the amount of jobs necessary to be added every month in order to keep the unemployment rate the same, has fallen by about half. For longtime readers who may have read something from me about U-Star (U*), this is a way of measuring it.

So the concern may truly still be only on the inflation side of the Dual Mandate. And that would mean keeping rates high.

But in 2025, trump doesn’t have an eye for objective, data-based reality. Instead, trump has an eye for winning, whatever the cost. So, install your own people at the statistical agencies to provide better numbers than exist in reality. Install your own people at the monetary authority to cut interest rates when the data tells you not to, in order to score political wins. And most of all, force the country’s apolitical backbone to bend to your political will. Control the narrative, and the population will believe you, even in the face of their own ruin.

If the new politicized era of US Economics is a basketball game, then we’re still in the first quarter of the trump 2 era. But if there is an interest rate cut tomorrow, as I am almost certain there will be, then the team will have settled in, made its first adjustments, and started matriculating the ball down the court. If we’re lucky, the shots will land and we’ll make it through the game clear and easy. But if things don’t go the admin’s way, if they have to make substitutions, or if other teams stop trading with them, then they’ll be forced to foul the other side (us). Let’s hope we don’t find ourselves there.

Discover more from The Millennial Economist

Subscribe to get the latest posts sent to your email.

Categories: Economics, Uncategorized

If prices are rising, then cutting interest rates would stimulate business investment, increase supply, to lower prices? Raising rates would hamper production increase?

Yahoo Mail: Search, Organize, Conquer

LikeLike